THE MORATORIUM POLICY- Loan EMIs & Credit cards Dues

Posted by Creditkaro

In one of our previous blogs, we talked about how the RBI

has announced a new monetary policy which includes a 3-month moratorium on all

payments which are outstanding as on 1st March 2020. The Reserve bank of India

allowed all the banks and NBFCs to give a 3-month moratorium on the repayment

of term loans like home loans, personal loans, educational loans, consumer

durable loans, automobile loans, and agricultural loans. According to the RBI,

all credit card dues and loan against credit card limit obtained before or on

1st march can also be repaid after the moratorium period is over, however, any

loan or credit obtained after 1st march is not covered under this policy.

Now, before you start celebrating it is particularly

important to know what exactly a moratorium period is and how you can smartly

use this time to save money and plan for future investments. The moratorium

period is just an EMI holiday and is a common practice during normal

circumstances as well.

A moratorium period is simply an EMI holiday which allows

you to have some time off before you start paying your dues. Under normal

circumstances, banks can offer you a moratorium period of up to 1 year in case

of Home and educational loans so that you can prepare yourself mentally and

financially to pay back the borrowed amount. However, simple interest is levied

on the loan amount during this time frame which is then added to the principal

amount.

So, before you get excited you must know that a moratorium period

is not something you can simply exploit. Instead, if you make good use of this

time, and use your funds smartly, you can enjoy financial stability for a

longer period.

Also Read: – RBI Monetary Policy: 3 Month Moratorium

The Reserve Bank of India (RBI) in a press conference on

27th March 2020 announced that all banks and NBFCs have been permitted to allow

a 3-month moratorium on repayment of loans outstanding on March 1st, 2020. So, there is an ample amount of time to

prepare yourself financially after this lockdown ends. If you think that this

just another holiday period and start taking your money for granted, then you

might soon find yourself in a debt trap.

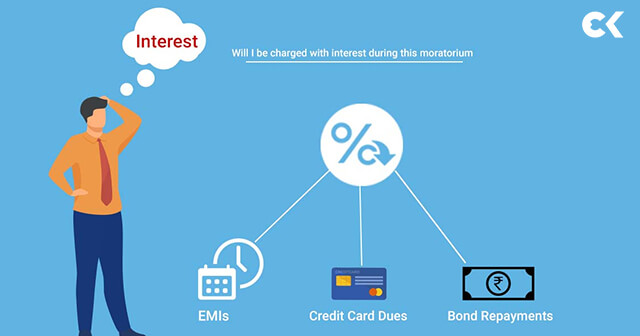

Will I be charged with interest during this moratorium?

Yes, RBI has clearly stated in their circular later that

interest shall be accrued on the outstanding amount of all term loans during

this moratorium period. The instalments have been deferred for the time being

but that is about it. Which means you will have to pay the following once this

period ends:

The most important thing for you to realize is that this

moratorium period comes to you at a cost, you have to pay the accrued interest

of these months and will have to pay it additionally with your regular EMIs.

Use this time to pay off other informal debts that might be pending. Payoff for other things that you were waiting for because this is a good time to do that. If not anything else, save more money during this lockdown period so that you can prepare yourself for the additional interest amount that you must pay alongside your principle amount.

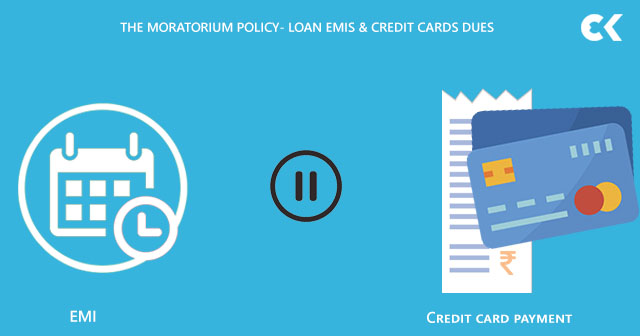

The RBI has made it clear that your credit card dues can

also be deferred during this moratorium period. Having said that, if you are a

cardholder then you need to remember that this moratorium will only delay the

payments for a while and the outstanding amount will continue to accrue

interest for the whole moratorium period.

So, when everything ends you will have to pay a higher amount than

usual. One good thing is you can apply for credit card at the comfort of your home. If you want to credit card apply online, click here

<a class="btn btn-info" href="https://www.creditkaro.com/credit-card">Credit Card Apply Online</a>

If you do not take this seriously today, you might push

yourself into a debt trap in the future, and an insolvency is very much likely,

given the fact that people are not getting paid or losing their jobs during

these times.

So, act smart, start saving money, start building funds, and

stay financially motivated. This an excellent time to spend more time with

yourself and your family, do that. Who knows you might realize an old talent

that could earn you some extra bucks!

Also read: – How to Keep Away From Financial Stress During Corona

Stay home, stay safe.

Category

Recent Post

Archive